Before you apply for your next credit card (or any loan, for that matter), you need to take specific steps to position yourself for a successful outcome — an approval with the best terms possible. Credit approvals do not happen by luck or mistake. They happen because you fit the profile of the type of customer that the bank is looking for. Here are 7 steps you need to take now so that you’re ready when you need to apply for credit.

What makes up your credit score?

Your credit score is based on a computer-driven calculation. Long gone are the days in which you had a conversation with your banker and they trusted you off a handshake and a “gentleman’s agreement.”

Credit scores are based on the following behaviors:

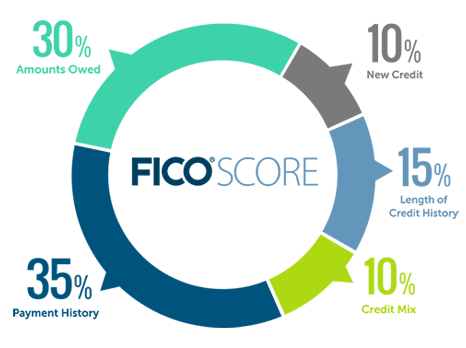

- 30% – Amount owed (utilization)

- 35% – Payment history (late payments)

- 10% – New credit (inquiries)

- 15% – Length of credit history (are your accounts new or old?)

- 10% – Credit mix (mixture of loans and credit cards)

MyFICO put together a great chart showing these components:

As you can see, 65% of your credit score is determined by your history of paying your bills on time (payment history) and your ability to keep your balances low compared to the credit limits you’ve been approved for (amounts owed).

Step 1 – Get your credit report and credit score for free

Congress passed a law requiring the three main credit bureaus (Experian, Equifax, and TransUnion) to provide consumers one free credit report each year from each of these providers. The best way to access your reports is through the government website – AnnualCreditReport.com.

The reports you get from AnnualCreditReport.com won’t include your credit score, but they will contain a LOT of valuable information. First off, make sure that you recognize all of the accounts. Fraud happens more often than you think! Second, make sure that the balances, payment history, and minimum payment are accurate. Sometimes, you will pay off a loan, but the bank will not update the credit bureau to show that the loan has a zero balance and has been paid off. Mistakes like this can negatively impact your ability to get approved for the credit you are applying for.

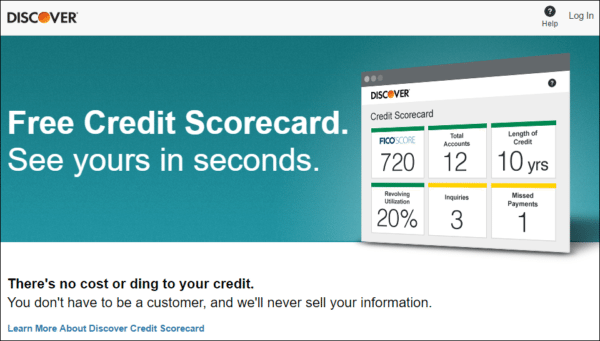

You can either pay the credit bureaus for your credit scores, or you can get them for free through a couple different ways. Sites like CreditKarma, CreditSesame, and Quizzle offer a free credit score that is updated on a regular basis. And more banks are offering free credit scores to their credit card customers. Bank of America, Barclays, Citibank, and Discover are just a few that offer this benefit. If you don’t already have a card with one of these cards, please use our referral link when you apply.

Recently, Discover started offering free credit scores to everyone… even if you don’t have one of their credit cards. Competition is fierce, and we all win when banks compete!

A point of caution. I’ve found that online free credit scores don’t always match up with the scores that banks use to determine whether to approve or decline your application. Treat these scores are directionally correct… and monitor them on a regular basis. If the score is going up, you’re doing the right things!

Step 2 – Take action to improve your credit score

Credit scores are like money. Not matter how much you have (or how high your score is), you always to be better. If you have a credit score of 740 or higher, you can get approved for most credit cards and you’ll get the best rates when applying for a mortgage or other loans. If your score is below that, or hovering nearby, then you need to take action to increase your score.

Credit scores are like money. Not matter how much you have (or how high your score is), you always to be better. If you have a credit score of 740 or higher, you can get approved for most credit cards and you’ll get the best rates when applying for a mortgage or other loans. If your score is below that, or hovering nearby, then you need to take action to increase your score.

One of my favorite tricks to increasing your score quickly is to pay off your small balances. And I’m not talking about after the statement arrives… I’m talking before the statement closes. The way credit reports work is that most banks report your balance as of the date of the statement, what your minimum payment is, your credit limit, and if you’ve paid on time. That’s it!

Because we’re smarter than the banks, we can implement a simple trick. Pay off as many of the small balances as possible before the statement closes. This will show a zero balance when the statement is published and your monthly minimum will also be zero. The more you can lower your balances and the more cards that you can show with a zero balance with no minimum payment, the better your score will be!

Common sense dictates the rest of your score. Continue paying everything on time and don’t apply for other credit until after you’ve been approved for the credit you really want. Friends in the mortgage industry have many unhappy stories about mortgages (home purchases and refinances) falling apart because people started applying for Home Depot and Lowe’s cards or running up balances buying new furniture before their home loan closed. Have patience people. Keep your eye on the prize… those lessser purchases can wait!

Step 3 – Prioritize what’s important to YOU

If you read travel blog websites or see commercials on TV, you’ll be bombarded with pitches why certain cards are perfect for you. That’s nice, but I don’t follow the herd in that thinking. Just because something is new, doesn’t mean that it is the right card for you.

For instance, I love Southwest Airlines, and I spend a lot of money on their card because the Companion Pass is my favorite benefit of any airline because it allows my wife to fly anywhere I fly for free. All I have to pay is the taxes on her tickets! However, if you want to fly to Europe, Southwest is not going to get you there, no matter how much you spend on their card.

Similarly, if you’re focused on buying a house in the next 6 months to 2 years, pursuing a credit card strategy to build up your miles and points balances to travel probably isn’t the best thing for you. You’re better off avoiding applying for credit until you’ve closed on your mortgage… then apply away for the cards you want afterward because buying the home is a higher priority to you.

Knowing what is important to you, and aligning your actions with your priorities will help your achieve your goals!

Step 4 – Know the rules of the game

The credit card industry is constantly evolving. Travel hackers develop strategies to maximize their ability to earn miles and points. Then banks look to cut off any strategies that become too unprofitable as they seek out long-term cardholders and people who spend “normally” on their cards.

There have been some significant changes in the last couple of years:

- American Express instituted a rule where you can only receive the bonus on a personal card once per lifetime. This was a rule that they had previously about 10 years ago.

- Chase implemented a “5/24 Rule” where they will not approve you for most cards if you’ve opened more than five new cards in the last two years.

- Citibank just launched a rule where you can only receive one bonus every 24 months per “family of cards”. For example, some of the families are ThankYou, American, and Hilton.

Since the Chase 5/24 Rule is the most impactful since they have some of the best cards, let’s discuss how this affects you. After you’ve reviewed your credit report, you’ll know how many new cards you have over the past 2 years. If you have more than 5 new accounts within the past 2 years, your chances of getting approved by Chase for a new card are basically nil. So, when you’re developing your card strategy, you know whether or not to apply for a Chase card based on how you stand.

Or, if getting a new card from Chase is your goal, like the new Chase Sapphire Reserve card and its 100,000 point offer (referral link), you may want to hold off on applying for cards from other banks or closing some other new cards, if it means you can get under 5/24 in a couple of months.

The good thing is that these restrictive policies are fluid. Often, banks will implement policies that are uber-restrictive only to realize that they were too tough and were cutting off too many customers. This will be especially true when the next recession hits and the banks seek to retain the most creditworthy clients with lucrative offers.

Step 5 – Business accounts are your friends

One of the quirks of the credit reporting world is that small business cards do not appear on your credit report. The only impact to your credit is that the inquiry for the small business card will knock your score down a couple of points and the inquiry will stay on your credit report for 2 years, but the actual account that you’ve opened doesn’t appear on the credit report.

One of the quirks of the credit reporting world is that small business cards do not appear on your credit report. The only impact to your credit is that the inquiry for the small business card will knock your score down a couple of points and the inquiry will stay on your credit report for 2 years, but the actual account that you’ve opened doesn’t appear on the credit report.

You may be saying to yourself, “but I don’t have a business.”

Well, you may be in business without really knowing it. Do you perform side jobs for others apart from your normal day job? Do you own rental properties, like I do? Do you sell crafts or other items on sites like Etsy or eBay? These are just a few examples, but each of these scenarios could be considered a small business!

Realize that you don’t need to have millions of dollars in sales to be qualified as a small business. In fact, if you’re just thinking about starting a small business, that’s reason enough to apply for a small business credit card. It is good practice to keep your personal and business expenses separate for accounting and tax purposes. Having a small business credit card from Day 1 of your small business will help you achieve the goal of keeping those expenses separate… and you’ll earn loads of extra miles and points in the process!!!

Since I’m over the 5/24 Rule with 8 new personal cards in the last 24 months, I’m actually going to focus solely on applying for business cards for awhile until I can get under the limit so I can get a new Chase personal credit card.

Step 6 – Selectively close accounts

15% of your credit score is based on the length of your credit history. Part of this score calculation factors in your oldest account, while another part of the score is based on the average age of your credit.

15% of your credit score is based on the length of your credit history. Part of this score calculation factors in your oldest account, while another part of the score is based on the average age of your credit.

With that in mind, if you close accounts that are newer than the average, this component of your credit score will actually increase. Your average age increases when there are more older accounts and fewer newer accounts.

When you combine this simple math with the Chase 5/24 Rule, you have a good reason to look at closing accounts that were opened in the last 24 months. I spoke with a few people in the Chase branches and they confirmed to me that Chase isn’t focused on the accounts that were opened in the last 2 years… instead, they are focused on the accounts that are still open from the last 2 years.

My conclusion is that Chase’s 5/24 Rule actually increases credit card churn, rather than minimizing it, because travel hackers are encouraged to close accounts shortly after they earn the bonus so that the new account doesn’t count towards the 5/24 Rule calculations. Chase could obviously change their application of the rule at any time, so be forewarned that this strategy would need to change along with it.

Step 7 – Take your time

Remember that travel and credit card hacking is a marathon, not sprint. Yes, it may stink if you can’t participate in the latest, greatest credit card offer, but there will be others.

Remember that travel and credit card hacking is a marathon, not sprint. Yes, it may stink if you can’t participate in the latest, greatest credit card offer, but there will be others.

Many cards offer increased bonuses on a regular basis. For instance, the Chase Southwest Visa offers 25,000 points regularly, but several times a year there will be offers for 50,000 points. You will kick yourself if you applied for the card and only received half of the points you could have received! By doing a little research and understanding whether a current offer is a good one or not.

Also realize that, while there are so many amazing credit cards available, you can’t get them all at once. Heck, you might not ever be able to get them all. This goes back to the point of prioritizing what’s important to you. Chase may have 15 or 20 cards that you’d love to have, but there’s no way you can have all of them… at least not all at once. I have 6 personal and 4 business cards with Chase, and I’m pretty maxed out with them.

Take it slow, and apply for a maximum of one personal and one business card per bank during your next “app party“. And don’t go hog wild and apply for 12 cards from an assortment of banks. Each inquiry, by itself, won’t impact your credit score much… but 12 of them at 2-5 points each, will do some serious damage to your credit score.

I apply for credit cards on a regular basis, and I only apply for 4 to 6 cards at a time every 4 to 6 months. That’s something you may want to work up to (or not). People learn to crawl before walking, and to walk before running. Start off with applying for 1 or 2 cards, see how it goes with meeting the minimum spends and ensuring that you’re not going into debt. Then you can try it again 6 to 12 months later.

Again, this is a marathon, not a sprint. You want to be in it for the long haul and by going too fast, too soon can ruin your credit and take you out of the game for years to come!

The Bottom Line

When applying for credit, you should do so with a strategy, not on an impulse. The best thing you can do is to implement your strategy now so that you’re ready to take action when the time is right. You don’t want to come across a once-in-a-blue-moon opportunity, that is only available for a short time, and then start the process. Prepping your credit for your next card application is not an overnight process. Follow these 7 simple steps and be ready to pounce!

")

Great stuff!

Thanks Randy. Especially with all of the craziness surrounding the Chase Sapphire Reserve card, I think people would have had much better success with their applications had they followed this approach.

I was declined for having 8 new cards in the last 2 years, so I’m positioning myself to get under 5 so I can reapply in a couple of months if the lucrative offer is still available.

Excellent primer! So clear and succinct, especially #6.

Here’s hoping peeps take this advice to heart!

Thanks Harlan! My background in banking definitely helps when understanding the credit process and what banks want to see with their credit applicants.